U.S. medical oxygen concentrators market to record substantial proceeds over 2018-2024, rising incidence of chronic respiratory ailments to drive the growth trajectory

Publisher : Fractovia | Published Date : 2017-02-22Request Sample

The accelerated pace of medical oxygen concentrators market share expansion can be primarily accredited to the rising prevalence of chronic obstructive pulmonary disease (COPD) coupled with escalating number of cigarette smokers across the globe. As per the estimates published in the Global Burden of Disease Study, a comprehensive report collated by World Health Organization, an overwhelming 251 million cases of COPD were recorded globally in the year 2016. In addition to this, a marked increase in the geriatric populace, that is prone to chronic ailments such as COPD and cystic fibrosis, has further augmented the growth prospects of medical oxygen concentrators industry in the recent years.

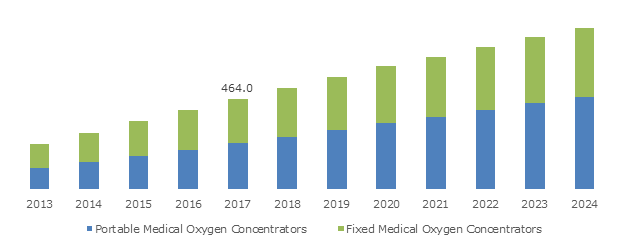

U.S. Medical Oxygen Concentrators Market, By Product, 2013 – 2024 (USD Million)

Elaborating further, the report, which assesses mortality and disability caused by major diseases, further claims that about 3.17 million deaths were caused by COPD in the year 2015 and 90% of these deaths apparently occurred in low and middle-income nations. The presence of higher amounts of smoke and dust across various industrial and manufacturing sectors has aggravated the levels of air pollution in emerging nations. Owing to the fact that people residing in such highly-polluted regions of emerging countries face an above-average risk of respiratory ailments, the commercialization potential of the medical oxygen concentrators market across these terrains can be termed as humongous.

Concurrently, it would be prudent to cite the efforts being undertaken by major companies to realign production strategies in a bid to solidify their stance in the global medical oxygen concentrators industry. One of the significant instances that needs mention is that of the United States based leading manufacturer of highly engineered equipment for energy and biomedical sector, Chart Industries Inc. Apparently, the firm had announced in 2016 that it would restructure its engineering and manufacturing operations within its BioMedical Group to acquire a significant portion of the ever-increasing medical oxygen concentrators market share in the ensuing years.

The company further declared to establish a Respiratory Center-of-Excellence in Georgia where manufacturing, marketing, and sales activities would be integrated to seamlessly deliver advanced oxygen concentrators to healthcare institutions. Taking into account the instance of Chart Industries it is quite apparent that prominent players in medical oxygen concentrators market are increasingly stressing upon strategic tactics like organizational realignment which would aid them in developing high-grade products in the times to come.

Additionally, it has been observed that globally renowned companies providing connected healthcare solutions for sleep and respiratory disorders have, of late, been focusing on acquiring upcoming firms operating in medical oxygen concentrators industry. Citing an instance of the same, the San Diego-headquartered ResMed, touted as one of the foremost innovators in offering respiratory and sleep-disordered breathing care, has concluded the acquisition of Texas-based Inova Labs in 2016 to enhance its existing product portfolio by adding novel portable oxygen concentrators.

For the record, Inova Labs is an emerging medical device manufacturer that specializes in developing state-of-the-art oxygen therapy systems. Reportedly, the latest takeover would assist ResMed in incorporating two of the most outstanding products of Inova Labs including industry’s first fully-integrated portable oxygen concentrator, Activox DUO2, and the lightweight portable oxygen concentrator with extended battery life, LifeChoice Activox.

Speaking of the regional growth outlook of medical oxygen concentrators market, the U.S. has been at the forefront of all the terrains apportioning a gigantic revenue share of about 88.1 percent of the overall business space in the year 2017. Apparently, such massive market share of the nation can undeniably be attributed to the escalating geriatric population coupled with increasing incidence of COPD in the recent times.

According to the findings of the leading national public health institute of the U.S., COPD was identified as the third leading cause of death in the country in 2014 with almost 15.7 million Americans reporting that they have been diagnosed with the ailment. Considering the escalation in the number of people affected by COPD and respiratory disorders, it is quite apparent that the commercialization potential of the U.S. medical oxygen concentrators industry can rightly be termed as humongous.

The rising occurrence of acute breathing ailments such as COPD, cystic fibrosis, and chronic bronchitis would undoubtedly propel the demand for oxygen concentrators in the forthcoming years. Driven by the increasing emphasis of government and private institutions to curb respiratory disorders, the global medical oxygen concentrators industry is slated to establish itself as one of the major verticals of the healthcare sector. The efficacy of these declarations can be affirmed by an estimation by Global Market Insights, Inc., which forecasts the overall remuneration portfolio of medical oxygen concentrators market to surpass USD 2.4 billion by 2024.