Metal and Ceramic Injection Molding Market to garner remarkable proceeds via latest tech innovations and strategic acquisitions over 2018-2025, Asia Pacific to steer the regional growth path

Publisher : Fractovia | Published Date : 2018-06-04Request Sample

Touted as one of the most under-rated niche verticals of advanced materials industry, metal and ceramic injection molding market has been progressing at a rapid pace over the recent years. Owing to the combination of both powder molded material and plastic molded design flexibility, this technology is being deployed massively to manufacture highly intricate ceramic and metal parts with exceptional strength and surface finish. In order to bring about a transformation in the traditional molding practices, the foremost players partaking in metal and ceramic injection molding industry have largely focused on swiftly adopting highly sophisticated molding technologies in the recent past.

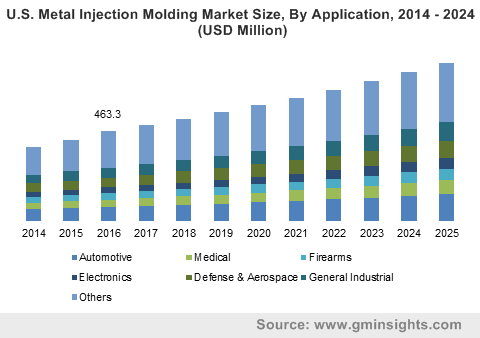

U.S. Metal Injection Molding Market Size, By Application, 2014 - 2024 (USD Million)

Citing an instance to validate the efficacy of the aforementioned statements, the United States based ceramic-injected components manufacturer, Scientific Ceramic Engineering (SCE), announced in 2016 that it has licensed a new ceramic injection-molding technology to provide customers with distinct advantages over traditional manufacturers. Apparently, the latest technology uses a lesser amount of toxic materials, low-pressure machinery, and room temperature molding method to manufacture robust and inexpensive complex ceramic components for a range of business verticals.

Concurrently, it is quite imperative to mention that the latest molding technique leverages the temperature flow properties of water-based ceramic suspensions and allows ceramic materials to be structured with higher accuracy. Moreover, the latest technology has been licensed from Purdue University’s Research Foundation Office of Technology Commercialization which is known to administer one of the most wide-ranging technology transfer schemes among prominent institutions of higher education in the U.S. Equipped with a set of novel properties and recognized by a reputed research university, the new technology is being referred by industry experts as unprecedented in the ever-evolving metal and ceramic injection molding market.

Strategic acquisition endeavors to galvanize the metal and ceramic injection molding industry share

In order to consolidate their profitability quotient and reach a wider consumer base, numerous established firms operating in metal and ceramic injection molding market appear keen on acquiring significant stakes in emerging companies. For instance, one of the foremost provider of advanced manufacturing and 3D printing solutions, ARC Group Worldwide, Inc., declared in 2014 that it has concluded the acquisition of a leading supplier of magnesium injection molding, Thixoforming.

Elaborating further, the takeover apparently supplemented ARC’s existing product portfolio with high-density injection molding components made of magnesium alloys and enhanced its injection molding suite of services. Similarly, the acquisition reportedly added an additional consumer base for ARC’s 3DMT division which would assist the firm in offering short-run production and prototyping services in the times to come.

Citing yet another instance of a crucial acquisition concluded recently, the China-based Nanjing Nangang Iron & Steel United Company Limited revealed in 2017 that it has purchased a majority stake in one of the leading firms across the Europe metal and ceramic injection molding market, Koller Beteiligungs GmbH. Apparently, the latest buy out would assist Nanjing Nangang in strengthening its product range with innovative lightweight products offered by Koller and manufacture high-quality solutions for the Chinese and Asian automotive market. For the record, Koller crafts injection molding composite components and pressing tools for a host of European automobile giants such as Land Rover, Mercedes, BMW, Audi, and Volkswagen.

Meanwhile, the regional growth outlook of metal and ceramic injection molding market is set to be led by the Asia Pacific region in the ensuing years. The burgeoning expansion of the several end-use segments of this business space such as electronics, medical, and automotive in the Asia Pacific realm can be accredited to the growing acceptance of these molding technologies. The swift rise of automotive sector across emerging economies such as India and China would consequentially propel the Asia Pacific metal and ceramic injection molding industry, which accounted for over 40 percent of the total remuneration share of this business space in the year 2017.

Primarily used to manufacture miniature products in various application segments along the likes of electronics, automotive, healthcare, aerospace, and defense, metal and ceramic injection molding technologies have transformed astonishingly over the past few years. The intensifying demand for complex parts that entail the deployment of high-performance materials, particularly silicon and stainless steel, would further fuel the remuneration portfolio of metal and ceramic injection molding market which has been forecast to surpass USD 4 billion by 2025.