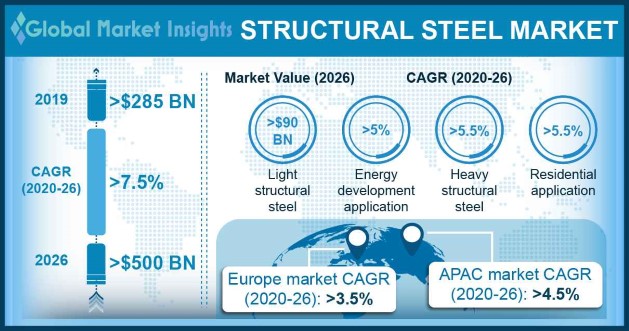

Europe structural steel market to accrue hefty proceeds by 2024, escalating construction of data center facilities to fuel the regional industry expansion

Publisher : Fractovia | Published Date : 2018-09-10Request Sample

Growing investments in the construction sector across the globe have provided a substantial push to the overall structural steel market, owing to the augmented demand for building materials that possess excellent strength and offer design flexibility. The remarkable malleability of steel and the precision with which structural steel can be shaped into a desired form allows engineers to realize innovative ideas and cater to wider applications. The structural steel industry has benefited from the development in off-site assembly of components, since pre-manufacturing of building parts reduces the erection time as well as labor costs.

Being considered to be more environment friendly to use, steel components can be recycled endlessly, without losing its properties, saving a lot of raw material in the manufacturing of recycled steel. Given additional advantages like resistance to fire and seismic activities, the structural steel market has enabled construction of durable buildings, bridges and roads in earthquake and flood prone areas across regions like Europe, U.S., South America and Asia.

US Structural Steel Market Size, By Non-Residential Application, 2017 & 2024, (Million Tons)

The European region is constituted of majorly developed nations that have enhanced infrastructure facilities and boast of extensive amount of funding available for commissioning residential and commercial expansion. The industry has been able to assist countries in erecting buildings that will not be easily destroyed during earthquakes, a quality which is necessary in some populated countries of the region that exhibit high risk of seismic activity. Subsequently, heavy sectional steel products have experienced massive consumption in the region for projects such as airports, retail malls, healthcare facilities and manufacturing plants. As steel does not hold moisture, European nations that are prone to floods demand heavy sectional steel structures to be of highly sturdy and durable. The Europe structural steel market has also gained prominence on account of the fact that a large portion of the continent is exposed to snowstorms and other hazards associated with harsh cold weathers.

Touted as one of the key steel-producing regions, Europe’s contribution towards the growth of the market from heavy sectional steel has been substantial due the presence of global manufacturers in the region. The world’s largest producer in terms of output, ArcelorMittal, earlier in January 2018 posted its highest third-quarter core profits from European operations since it initially started reporting them combined from 2014. Salzgitter, Germany’s second biggest steel producer, had also reported its best nine-month figures since 2008, with industry experts suggesting that the margins for the overall structural steel industry could surge further. Having enough production capacity to fulfil the needs of extensive construction projects across the globe, European companies are able to support the region’s infrastructure development with cost-effective and high quality steel components.

The heavy sectional steel demand in Europe has not only seen a sharp rise from the construction of healthcare facilities, airports and extension of manufacturing plants, but also from the growing need for data centers. Increasing preference of organizations towards integrating their processes with the cloud for achieving low-cost optimization and control has proliferated the structural steel market. A recent survey conducted among respondents from the data center segment revealed that about 19% of them own 10 or more data centers whereas 58% owned 2 to 9 facilities. The rapid developments in edge computing will lead to the establishment of more centers in the coming years, which would eventually boost the industry. In the survey, nearly 50% of the respondents said that their data centers would be between 5,000 square ft. to 50,000 square ft. over the coming 12 months, while 26% respondents believe their data centers could be between 100,000 square ft. to 500,000 square ft. over the next three years.

As evident, the construction of data centers is bound to increase in the near future and with an advanced technology base, Europe will also exhibit a tremendous affluence in terms of providing cloud and edge computing services. This will benefit Europe’s structural steel market as heavy sectional steel components allow for building a 100 percent clear span design, providing more room for computing equipment and servers. These materials have excellent fire resistant properties and adding insulation or atmosphere control systems is easier, besides offering cost advantages due to faster erection and reduced spending on labor. Since such facilities are being built not just in major cities but also in remote locations, organizations have been planning to erect steel structures that are robust, enabling the incorporation of essential features.

All in all, the global market will witness enormous gains from the demand for heavy sectional steel from the building and construction sector. Driven by the efforts of prominent industry participants such as ArcelorMittal, Hunan Valin, Shagang Group, Nippon & Sumitomo Metal Corporation, Tata and POSCO, global structural steel markets size will be pegged at an astounding USD 850 billion by 2024.