U.S. oil and gas infrastructure market valuation to surpass $80 billion by 2024, surging government initiatives to add impetus to industry growth

Publisher : Fractovia | Published Date : 2018-12-31Request Sample

The fact that the U.S. oil and gas infrastructure market is expected to do exceptionally well over 2018-2024 has been underlined by the fact that recently United States has begun exporting more oil than it imported, a phenomenon that has occurred for the first time in the past 75 years. This is a significant milestone for not only the Trump administration that has increased oil and gas sales to rebalance trade and diminish the gap between what the country buys from foreign countries and what it sells but also in the resurgence of domestic energy production. More importantly, it is an indicator for the future growth prospects of the U.S. oil and gas infrastructure market that is expected to record an unprecedented surge in the ensuing years.

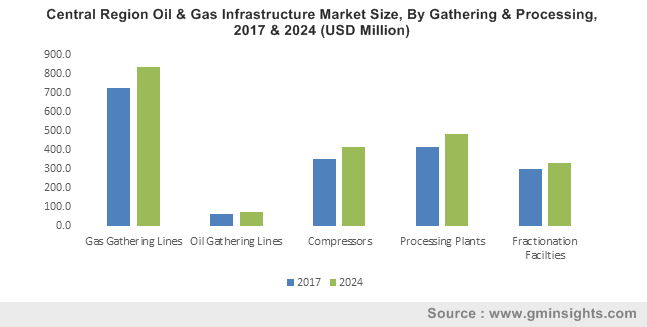

Central Region Oil & Gas Infrastructure Market Size, By Gathering & Processing, 2017 & 2024 (USD Million)

In 2018, United States surpassed Russia as the largest oil producer in the world. Developments in the U.S. oil and gas infrastructure market as well as technological improvements have helped in the doubling of domestic production over the past decade and facilitated the extraction of oil from shale formations while natural gas production has also been increased drastically. Government initiatives like lifting a longstanding ban on crude oil exports in 2015 has allowed the United States to take full advantage of the increase of domestic production and selling of these products across borders.

Sale of crude oil as well as refined products such as gasoline have apparently shifted the balance of energy imports and exports in favor of the U.S. Even a decade back, net energy imports equaled more than a quarter of domestic energy consumption but in 2018 the figure fell by 5% and according to the Department of Energy, United States is expected to become a potential net energy exporter by 2022, encouraging investors to add momentum to the U.S. oil and gas infrastructure market.

Major ripples of anticipation have also been created in the U.S. oil and gas infrastructure market as the United States Geological Survey (USGS) declared the discovery of colossal oil and gas reserves in West Texas’ Permian Basin. As per to the USGS, an enormous 46.3 billion barrels of oil, 20 billion barrels of natural gas liquids and 281 trillion cubic feet of natural gas have been discovered in the Texas and New Mexico’s Permian Basin. Key players in the energy industry have established a significant presence in Bone Spring and Wolfcamp areas around which areas the discovery is centered, and it is well known that the fields were remarkably fertile grounds for oil extraction. However, the sheer new figures are apt indicators of the progressive path that the U.S. oil and gas infrastructure industry is likely to traverse on.

Such figures also come at a favorable moment for the U.S. oil and gas infrastructure industry to find greater growth encouragement both from private investors, industry players and government bodies as Europe is looking to lower its reliance on Russian oil and natural gas. Despite the push to get off fossil fuels, Europe's gas needs have not witnessed a decline in recent years. In fact, in 2017, Europe’s gas demand has been the highest since 2010 and over the past three years, gas consumption has been recorded to surge by approximately 20%.

The International Energy Agency reports that gas now fulfills nearly 24% of energy needs in Europe and is estimated to rise to approximately 30% in the years ahead as nuclear, oil and coal confront a gradual reduction in market share. For instance, gas power generation capacity will increase from about 270 GW to almost 390 GW by 2040. With the U.S. having bourgeoning number of LNG export terminals along the Gulf Coast, it is clearly one of the foremost choices for Europe to source its gas requirement, in turn adding impetus to the U.S. oil and gas infrastructure industry.

The shale gas windfall that U.S. has witnessed in the past decade has eventually led to a massive surge in cheap natural gas which has led to increased gas-fired generation and LNG export terminals besides a proliferation of processing facilities, pipelines and chemical complexes. Much of the gas is sourced from the Marcellus and Utica Shales in West Virginia and Ohio. Besides burning this gas for heating and electricity, a major volume of the gas is also used in the manufacturing of fertilizers and plastics. In an initiative to develop a hub for plastics and other petrochemical products in Appalachia, outside of Pittsburgh, the Royal Dutch Shell has given the ethane cracker facility in question the greenlight and $6 billion have been allotted for the development.

The federal government is also working to make the development a success while the Department of Energy published a report for the U.S. Congress promoting the case for a new petrochemical hub. With the government as well as environmental agencies encouraging such developments, the U.S. oil and gas infrastructure market is expected to register colossal growth over 2018-2024.