GaN and SiC power semiconductor market to derive extensive proceeds from solar energy deployment through 2025

Publisher : Fractovia | Published Date : 2019-07-12Request Sample

Driven by the increasing deployment in renewable energy applications, GaN and SiC power semiconductor market is fast emerging as a profitable niche vertical of the global electronics and media industry. Silicon carbide and gallium nitride are becoming more popular across various business sectors owing to the fact that conventional silicon-based devices are reaching their material limits. This has specifically resulted in increased uptake of these semiconductors by renewable energy sector.

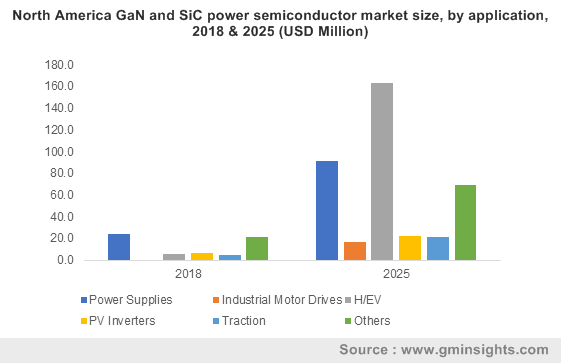

North America GaN and SiC power semiconductor market size, by application, 2018 & 2025 (USD Million)

The power semiconductors possess more thermal energy and wider bandgap which makes it an ideal substitute for silicon as it can withstand high voltages and temperatures. Owing to these features, GaN and SiC power semiconductors are finding their applications in areas such as UPS, hybrid and electric vehicles, and more importantly in PV inverters.

Prominent semiconductor manufacturers like Infineon are making big-ticket investments to upgrade existing technology – a factor that is likely to favor GaN and SiC power semiconductor market share.

The overall product demand would be significantly impacted by the shifting focus of economies toward the installation of renewable energy plants to support sustainable development. Numerous American, Asian, and European nations comprising of the U.S., Mexico, China, India, Sweden, Norway are formulating energy policies which rely heavily on renewables. Moreover, these nations are investing massively in the development of commensurate renewable energy infrastructure.

Solar energy has emerged as one of the fastest growing renewable energy sources across the world. In order to make solar energy more accessible and explore strategies for development and deployment of renewables, developed and emerging nations are joining forces to establish global platforms in the recent past. International Solar Alliance (ISA) is one such global initiative which represents the future energy scenario and would prove to be crucial in the overall renewable revolution. Since GaN and SiC power semiconductors are primarily utilized in the PV inverters, initiatives like ISA would be instrumental in attracting massive investment in solar energy sector which will indirectly support the market trends.

In terms of geographical expansion, GaN and SiC power semiconductor market outlook is gradually changing in the developing countries of the Asia Pacific region such as India and China. The presence of large solar facilities is the most significant factor that has increased product demand in these nations. To put things into perspective, China has more solar energy capacity – a humongous 130 gigawatts – than any other nation in the world. It is home to the largest solar facility in the world – the solar plant in its Tengger Desert with a capacity of more than 1,500 megawatts. Moreover, China has many sizeable solar farms including the massive 850-megawatt Longyangxia Dam facility on the Tibetan Plateau.

India is also witnessing exponential increase in demand and supply of renewable energy. Proactive government initiatives and policy support to develop and deploy solar energy facilities makes it one of the world’s largest green energy markets. After allowing 100 percent FDI in solar energy plants, the government of India is now aiming to surpass the set target of 175 gigawatts of renewable energy capacity by 2022.

When compared to conventional silicon-based semiconductor devices, GaN and SiC semiconductor materials can be utilized in smaller, faster and more reliable energy systems that can increase their effectiveness and productivity. In fact, these semiconductors can reduce approximately 90 percent of the energy losses during power conversion. Taking into account these unique abilities, several automation firms are also incorporating GaN and SiC power semiconductor in various industry applications.

Increased formulation of policies – directed toward mitigation of greenhouse gas emissions – has given rise to installations of photovoltaic inverters. These policies endorse a clean environment which would support sustainable development across the world. Moreover, these policies will improve GaN and SiC power semiconductor industry outlook over the years ahead. NXP Semiconductors, ROHM Semiconductor, Infineon Technologies AG, and Mitsubishi Electric Corporation are some of the mainstream firms constituting the competitive hierarchy of the industry. Reports forecast that the remuneration scale of GaN and SiC power semiconductor market is likely to surpass USD 3 billion by 2025.